.png)

.png)

In the early 2020s, "Dunning" was synonymous with payment recovery. It was a simple, loud process: a payment fails, the system sends three emails over ten days, and if the customer doesn't update their card, they are out.

By 2026, that model has become a liability for B2C brands.

For a consumer paying $14.99 for a fitness app or a streaming service, a "Payment Failed" notification is less of an invoice reminder and more of a friction-filled roadblock. In a world of subscription fatigue, the moment you ask a customer to perform a manual task like logging in or finding their wallet, you risk them getting distracted or simply forgetting to follow through.

The data is clear: Involuntary churn (failures due to technical issues or temporary card limits) accounts for up to 40% of all churn. Addressing this requires a move away from "Generalist" tools built for B2B invoices and toward AI-first, "Silent Recovery" engines that fix the plumbing without bothering the tenant.

A lot of teams start by using the native tools provided by their payment processor, such as Stripe Smart Retries. While these are convenient, they are generalist solutions designed to work for everyone from a local plumber to a B2B enterprise. Because they serve a massive, diverse user base, native tools prioritize broad compatibility over the deep optimization required for high-growth consumer apps.

For B2C brands, this often means your recovery logic is optimized for "average" global success rather than the specific patterns of a mobile-first subscriber. Even the best failed payment recovery tools struggle to perform when limited by the rigid rules of a standard payment processor. Using a native platform alone essentially forces you to accept a "good enough" recovery rate that inevitably leaves six or seven figures of revenue on the table as you scale.

Dedicated failed payment recovery tools focus exclusively on the mechanics of failed payments, allowing them to iterate on features far faster than a massive payment processor. While native platforms often stop retrying after a hard decline or a set number of days, standalone tools like Redux use specialized machine learning trained on millions of B2C transactions to identify declines that native tools miss.

These dedicated engines can navigate complex payday cycles and banking windows that a generalist tool simply isn't programmed to look for. Furthermore, the best failed payment recovery tools offer more robust analytics, showing critical data like trial-to-paid recovery rates. By focusing on a specific vertical, standalone tools transform payment recovery from a passive billing task into a strategic revenue-generating engine.

| Tool | Recovery Method | Best For | Key Standout Feature | Pricing Model |

|---|---|---|---|---|

| Redux Payments | Silent-First AI | B2C Apps, Streaming & Consumer SaaS | AI retries, Trial-to-Paid Optimization & No-Login Magic Links | Pay-on-Lift (Zero Risk) |

| Butter Payments | Gateway Optimization | High-volume subscription & technical glitches | Technical "Retry" timing at the bank level | Revenue Share |

| Churnkey | Retention Hybrid | Brands with high voluntary churn | Dynamic "pause" and "discount" save flows | Monthly MRR-based tiers |

| Churnbuster | Multi-Channel | Shopify & eCommerce (Physical goods) | Advanced SMS & Email recovery sequences | Monthly Tiered Subscription |

| Stripe Smart Retries | Native Baseline | Small businesses & startups | Built-in convenience; zero setup required | Included in Stripe Billing |

| Revaly | False decline AI | High-volume subscriptions with "False Declines" | Specializes in reversing false declines | Pay-on-Lift / Custom |

| Paddle Retain | Benchmarking AI | Companies in the Paddle ecosystem | Uses cross-platform data for recovery logic | % of Recovered Revenue |

| Vindicia Retain | Enterprise Legacy | Fortune 500 & Global Media | High-density global regulatory compliance | Custom Enterprise Contracts |

Redux Payments is an optimization layer designed specifically for the Stripe ecosystem. While Stripe provides the rails, Redux provides the high-performance engine required for B2C scale. Most failed payment recovery tools are generalists that treat a terminal $2,000 B2B failure the same as a $20 B2C "soft" decline. Redux treats these B2C failures as high-probability recovery signals, utilizing machine learning to navigate consumer spending cycles and bank-level limits.

Pros:

Cons:

Most native billing systems use a static, one-size-fits-all retry ladder. They treat a $699 B2B subscription that failed because the employee left the company exactly like a $39 fitness subscription that failed for insufficient funds. This leads to aggressive retries that trigger fraud blocks and missed recovery windows.

Traditional dunning relies heavily on "Payment Failed" emails that force customers to log in and manually update their cards. This creates a massive friction point where users drop off simply because the process is too cumbersome.

Native platforms like Stripe have a major reporting blindspot: they don't clearly show "trial-to-paid" recovery rates. This leaves high-growth apps blind to how much revenue is lost at the most critical stage of the customer lifecycle.

Redux provides a comprehensive, tiered AI orchestration approach that scales with the complexity of the decline.

Redux Payments consistently outperforms Stripe Smart Retries through a Tiered AI Orchestration approach that captures the involuntary churn native logic misses. By splitting recovery into Silent Recovery for soft declines (utilizing proprietary payday-matching) and Active Recovery for hard declines (leveraging frictionless Magic Links), Redux delivers a 20-30% average incremental lift. This specialized engine is proven to secure the trial-to-paid gap for B2C leaders, with verified benchmarks including a 134% increase for Cramly (8% total ARR boost), a 132% increase for Knowt, and a 36% boost for Autopilot.

Redux is an Official Stripe Partner, verified within the Stripe Partner Directory. This status ensures our platform maintains the highest level of API fidelity and security vetting required to operate as a native extension of Stripe Billing.

Autopilot, a viral fintech platform with over $1bn AUM, faced a critical challenge: explosive growth led to thousands of failed payments that were slipping past Stripe's native tools.

The Results:

Stop losing revenue to accidental churn. Start your zero-risk pilot with Redux Payments today and only pay when we outperform your current baseline.

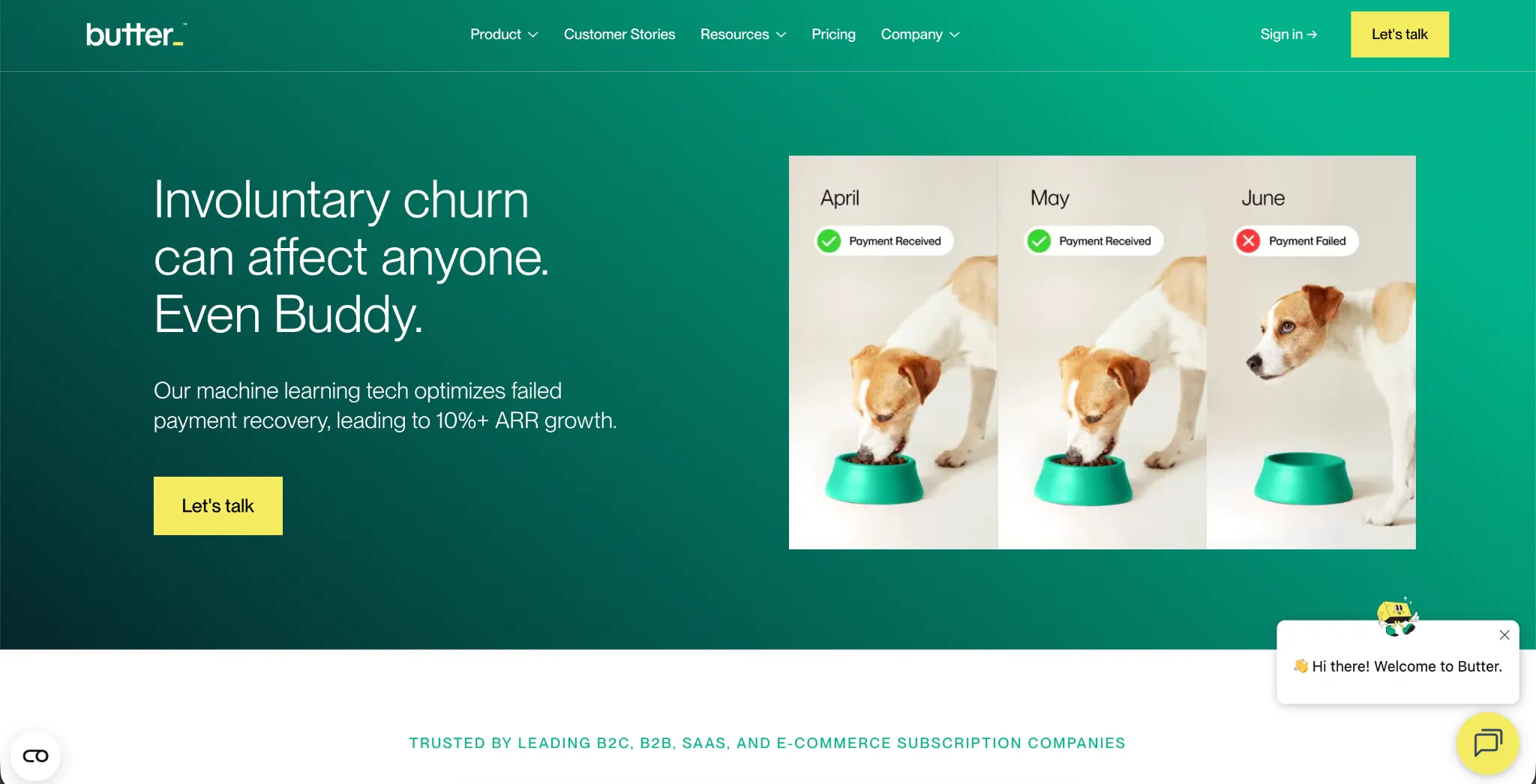

Butter Payments takes a heavy data-science approach to the "retry" by focusing on the technical conversation between the merchant and the issuing bank. They use data to time their payment attempts for the exact moment a bank’s system is most likely to approve the transaction, avoiding periods of high-traffic or technical downtime. As one of the best failed payment recovery software tools for gateway optimization, Butter is highly effective at solving technical errors and bank-level connectivity issues that lead to accidental churn at the gateway level.

Pros:

Cons:

Pricing:

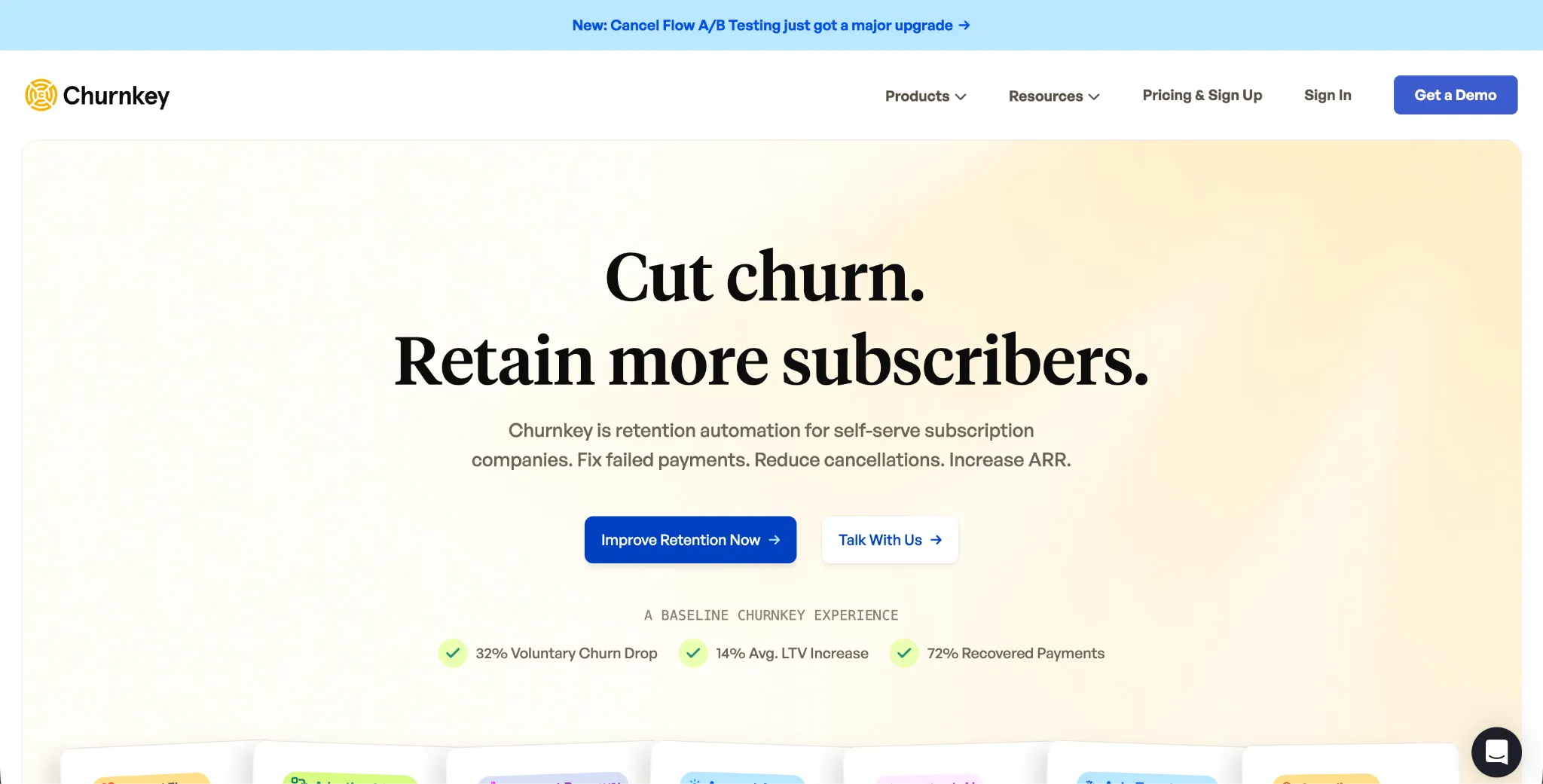

Churnkey has evolved from a voluntary churn "cancel survey" into a "jack of all trades" for retention and revenue stability. While they remain famous for their cancellation save flows, they now offer a robust involuntary churn suite featuring Precision Retries and in-app payment walls. Their platform leverages vast benchmarking datasets to group retry attempts by decline type, intelligently handling insufficient funds and "try again later" codes. Their approach makes them a strong choice for SaaS companies that want a single dashboard to manage both customers trying to leave and payments that are failing quietly.

Pros:

Cons:

Pricing:

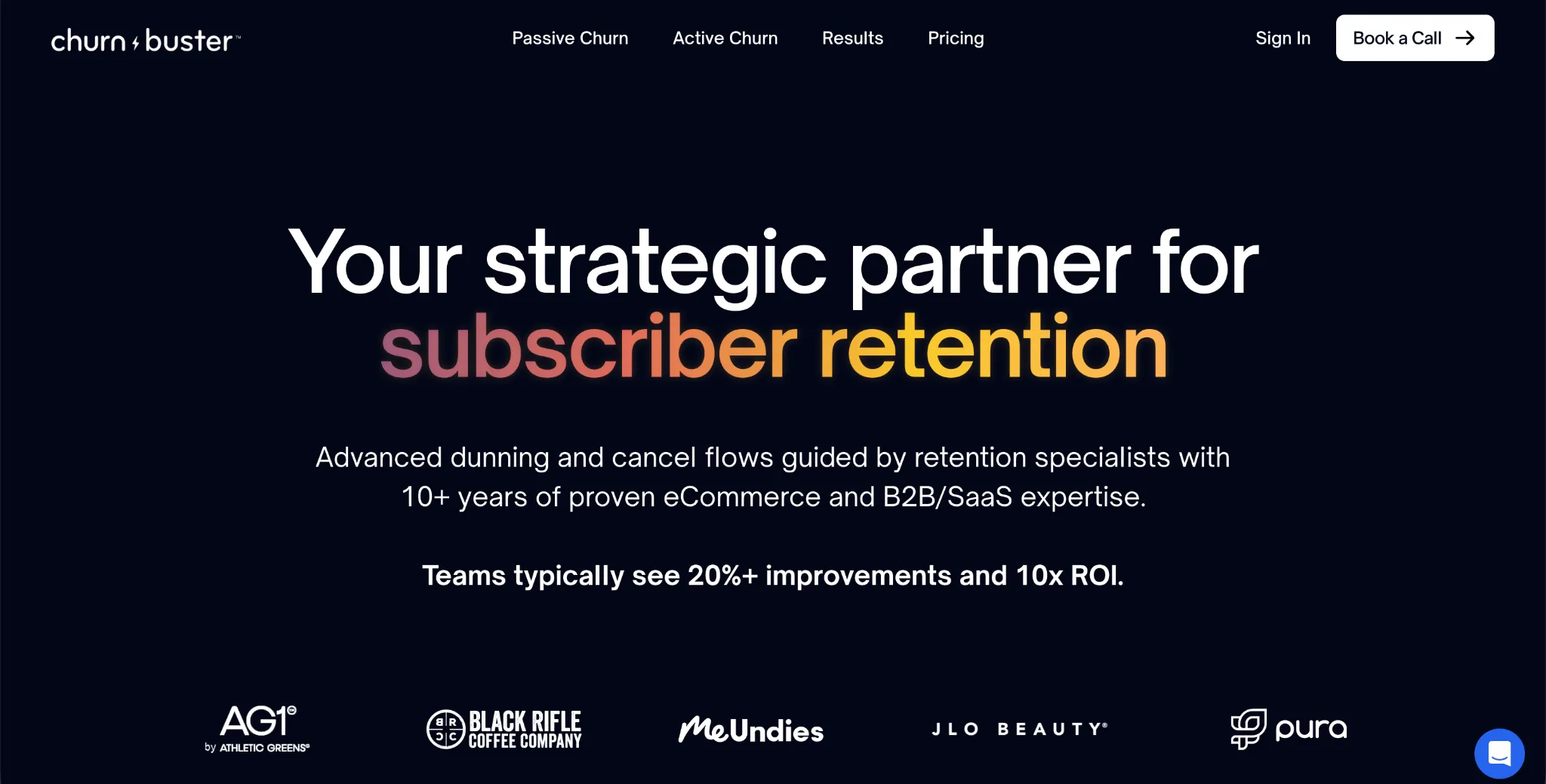

Churn Buster is the primary choice for eCommerce brands operating on platforms like Shopify or Recharge. They provide immediate, granular control over the active recovery phase, offering robust SMS and email sequences that help resolve "soft declines" for physical goods. While many failed payment recovery tools focus on the API, Churnbuster excels at multi-channel communication that brings customers back into the fold when a package doesn't ship, allowing temporary issues like daily spending limits to settle before launching automated campaigns. Their core strength remains in high-visibility, multi-channel communication that brings customers back into the fold.

Pros:

Cons:

Pricing:

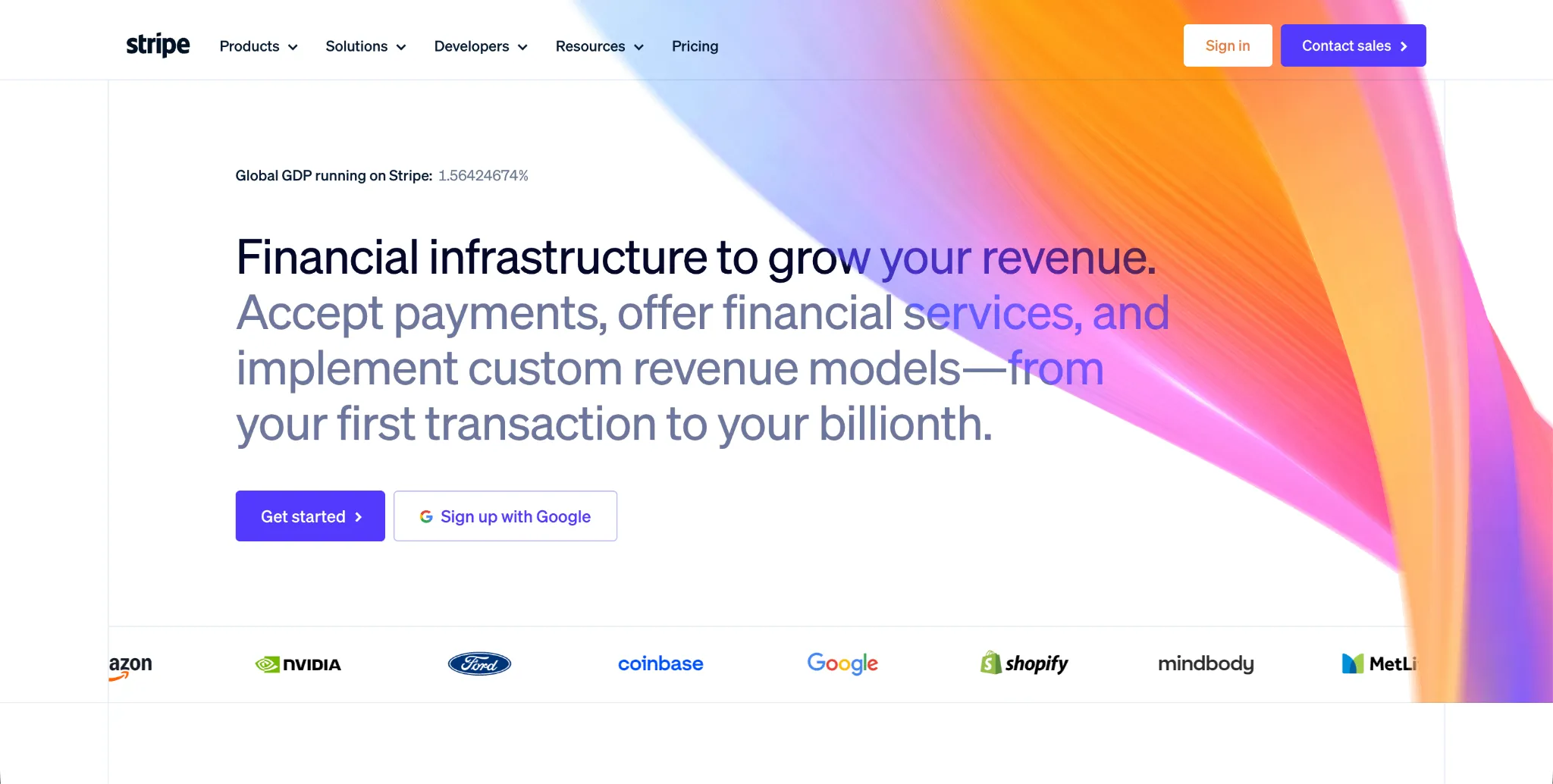

Stripe Smart Retries uses machine learning trained on billions of data points to determine the best time to retry a payment. It serves as the baseline for most subscription businesses, offering a "set it and forget it" foundation that recovered over $6.5 billion in revenue for users in 2024. However, because it is built to serve every type of business globally, it often lacks the specialized depth required to capture the final 20-30% of revenue that the best failed payment recovery software tools can find. Most growing brands use Stripe as their floor and layer a specialized tool like Redux or Butter on top to maximize their "Trial-to-Paid" conversions and consumer failed payments.

Pros:

Cons:

Pricing:

Revaly (Formerly FlexPay) utilizes its AI engine to provide a payment intelligence layer that specializes in reversing false declines. Their core strength lies in distinguishing between actual fraud and false positives, which are legitimate transactions that banks mistakenly block. By analyzing deep historical data and issuer behavior, Revaly salvages these transactions at the bank level, often before the customer even knows there was an issue.

Pros:

Cons:

Pricing:

Formerly known as ProfitWell Retain, this tool is now integrated into the Paddle ecosystem. It leverages massive benchmarking data sets from thousands of SaaS companies to optimize recovery. It is a strong choice for companies already using Paddle for global tax and billing compliance who are looking for reliable failed payment recovery tools with a hands-off approach.

Pros:

Cons:

Pricing

Vindicia is a long-standing retention and subscription management platform focused on the high-volume digital media sector. The infrastructure is engineered to process millions of transactions while managing complex global banking and regulatory compliance requirements. It is positioned as a legacy-scale option for Fortune 500 corporations that require standardized security protocols and consistent performance for high-density subscription models.

Pros:

Cons:

Pricing:

In 2026, "Static Dunning" (sending emails on day 1, 3, and 5) is considered legacy tech. Modern B2C success depends on Predictive Authorization.

When a card fails, it isn't always because the customer has no money. It could be:

Redux Payments and other AI-first tools use these signals to time retries. If a retry happens at 2:00 AM on a Tuesday when the bank's after hours fraud filters are higher, it might fail. However, if that same transaction is processed during normal business hours on a Friday payday, it’s far more likely to be approved. By timing the attempt correctly, the payment is recovered through the silent recovery process, ensuring the customer never even knows there was a problem.

Before selecting a recovery partner, ask these three questions:

Dunning software automates the process of recovering failed subscription payments. It replaces manual email follow-ups with intelligent retry logic, card update flows, and customer outreach to reduce involuntary churn and recover lost revenue.

For B2C subscriptions on Stripe Billing, Redux Payments offers the highest recovery lift with AI-powered retry timing, silent recovery, and instant card update flows. It layers on top of Stripe Smart Retries and only charges on incremental revenue recovered above your Stripe baseline.

AI payment recovery analyzes transaction-level data including decline codes, bank behavior, cardholder patterns, and time-of-day signals to determine the optimal moment to retry a failed payment. Unlike static retry schedules, AI models like Redux adapt per-transaction, which leads to 20-30% higher recovery rates compared to default processor retries.

Most dedicated recovery tools recover between 25-50% of failed payments for B2C that would otherwise be lost. Results depend on your subscriber base, payment method mix, and decline code distribution. Redux Payments customers typically see a 20-30% improvement over their Stripe Smart Retries baseline.

Traditional dunning sends emails and notifications asking customers to update their payment method. Silent recovery fixes failed payments in the background through intelligent retries and network-level card updates without ever contacting the customer. Silent recovery preserves the customer experience and avoids the unsubscribe risk that comes with dunning emails.

Pricing models vary. Some charge flat monthly fees ($29-$500/mo), while others use pay-for-performance pricing where you only pay a percentage of recovered revenue. Redux Payments uses a pay-on-lift model where you only pay on incremental revenue recovered above what Stripe already recovers for free.

Involuntary churn happens when customers lose access to their subscription due to a failed payment rather than a deliberate cancellation. Industry data shows 20-40% of total churn is involuntary, costing the average B2C SaaS company 4-8% of MRR annually. For a company doing $20M ARR, that's $800,000-$1,600,000 in preventable revenue loss per year.

The evolution of payment recovery in 2026 has revealed a hard truth: in the B2C sector, customer attention is your most expensive resource. Traditional dunning tools treat failed payments as a customer service issue. At Redux Payments, we treat them as an engineering optimization problem. The data proves that "Generalist" tools like Stripe Smart Retries, while competent, are not calibrated for the specific volatility of consumer liquidity and issuer behavior. By applying a Silent-First methodology, we effectively decouple payment success from customer effort.

The result is a recovery engine that doesn't just "save" subscriptions, it also protects the brand relationship. With a Pay-on-Lift model, the transition to AI-driven recovery isn't just a technical upgrade; it is a fiduciary imperative. For B2C brands, the best failed payment recovery tool isn't the one with the best emails, it's the one that ensures those emails never have to be sent.

Ready to see your recovery potential? Start your zero-risk pilot with Redux Payments today

.svg)

.svg)

.png)